Emerging markets face multiple tantrums

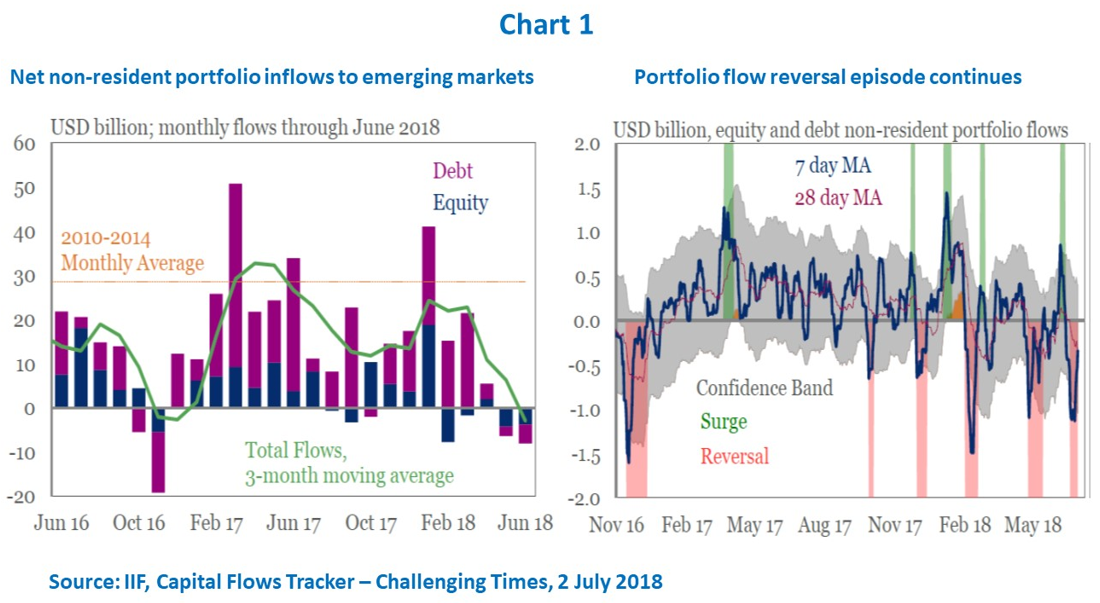

The addition of a fourth US rate rise to the Federal Reserve’s 2018 dot-plot graph after the June meeting of the Federal Open Market Committee sparked a bout of portfolio outflows from emerging markets. This followed a fleeting upswing at the beginning of the month that fell short on reversing the unwinding of exposure and sell-off of assets in May (Chart 1). Country differentiation has been accentuated, with exchange rate devaluation pressures and capital outflows occurring more notably in economies exhibiting higher vulnerability to sudden stops in foreign finance.

Since April I can single out at least three different factors that have led to sudden bursts of fears among investors of losses in portfolios in individual emerging markets. First, there is the ‘dollar tantrum’. Argentina and Turkey were the two major cases of a rout in May, and they entered the current phase of rising US Treasury yields and dollar values sharing weaknesses. Their current account deficits had deteriorated substantially in the recent past. Since the 2013 ‘taper tantrum’, Argentina’s current account deficit has jumped to levels comparable to those of the then ‘fragile five’ (Brazil, India, Indonesia, South Africa and Turkey), while Turkey was the only one among the five countries to have remained there. In both cases, inflows of foreign direct investment fall significantly short of covering the gap in the basic balance of payments. Because of structural current account deficits that are not financed by FDI but rather by hot capital inflows, both countries have featured low levels of reserve adequacy.

Another common feature they share is that their dollar-denominated debt as a share of GDP makes them more fragile in the light of the dollar’s strength over recent months, while corresponding debtors in both economies do not have a ‘natural hedge’ in terms of dollar revenues. Ultimately, currency mismatches on dollar-denominated debtors’ balance sheets have made them prone to shocks arising from dollar strengthening.

This combination of dollar-denominated debt and low levels of reserve adequacy in Argentina and Turkey made both economies highly sensitive to the effects of the mid-April US Treasury yield spike. Under such circumstances, any events seen as undermining commitment to appropriate policies could trigger an unwinding of positions by asset holders. This occurred in both countries amid rising doubts about their commitment to monetary policy targets.

Second, there is the impact of a ‘political tantrum’ on capital outflows and exchange rate depreciation pressures in Mexico and Brazil. For the latter, although balance of payment conditions are relatively sound and confidence in monetary policy is high, prevailing fiscal trends highlight Brazil’s weakness in the absence of public expenditure reforms. Recent polls unfavorable to candidates committed to such reforms who will stand in October’s general election have fed fears that led to portfolio rebalancing away from Brazilian assets. In response, the central bank sold a large amount of local currency-denominated foreign currency swaps to allay volatility and capital outflows.

A third source of shock is a ‘trade tantrum’. Concerns about spillovers from the US-China trade war on global value chains have affected asset values in some Asian economies.

"The trade war between the US and China, as well as uncertainty regarding the ability to accomplish fiscal reforms in Brazil for instance, have exacerbated the risk of rebalancing investors’ portfolios away from emerging markets assets"

Raft of risks

The baseline scenario for emerging markets is that GDP growth is likely to decelerate in the near term. Portfolio rebalancing and exchange rate realignment tend to worsen the growth-inflation trade-off. Heavy dependence on continued external financing is concentrated in just a few emerging markets. Only a few countries have balance of payments deficits that point to critical vulnerabilities, and overall reserve adequacy is close to its record high. To some extent, the weight of FDI in the composition of capital flows should make emerging markets more resilient against the impact of global portfolio rebalancing.

This view is subject to several risks associated with further US yield spikes and dollar appreciation. Investors will need to remain aware, too, of the effects of the Fed’s balance sheet unwinding, in tandem with rising US bond issuances. Depending on financial market conditions and risk appetite, there might be some crowding-out pressures on emerging market bond holdings, particularly if the Fed decides to speed up its balance sheet ‘normalization’.