Potash: a typical price war

A growing world population, changing food demand favoring protein, and limited agricultural supply under the assumption of constant returns: these are three key variables of a complex equation that could explain why fertilizer demand should increase structurally in the coming decades. Although the various existing fertilizers may share common demand factors, they are characterized by multiple pricing dynamics due to differentiated supply factors. A fertilizer is comprised of three main nutrients nitrogen (N), phosphorus (P) and potassium (K) in varying proportions, and thus form so-called binary or ternary fertilizer used according to the nature of crops and soil types. To the extent that these components do not have a common geographical origin, are not extracted or processed by the producers themselves and do not have the same costs of production structures, it is customary to differentiate their markets. Traditionally, a distinction is made between the markets for potash, urea (the main nitrogen fertilizer) and phosphate.

For fertilizers, the potash market is probably the one that has generated the most interest among researchers in economics over many decades. Several intertwined reasons help to explain this. First, potash is a strategic raw material for the United States. The mining industry has certainly existed on the North American continent since the early twentieth century, but at insufficient production levels to meet growing agricultural demand. The largest deposits are located in Germany, and their mines contribute to the success of German agriculture. On the eve of the First World War, Germany’s near monopoly, however, raised U.S. concern, as the world's second largest potash consumer. It also raised the interests of economists, such as Tosdal (1913), who research about the effects of Germany’s regulations. History confirmed this concern. As evidenced by the chart below, the price of potash indeed peaked in 1916 at nearly 7,500 USD (1998 dollar equivalent) following the suspension of German exports with the United States’ impending entry into the war.

Figure 1: Evolution of potash prices in the US (In constant 1998 USD, 1900-2013)

Source: United States Geological Survey

In addition, the potash market has long been seen as an illustration of the concept of "imperfect" competition due to the historical existence of production cartels. Like Tosdal, since 1942 Hayes has been looking not only at the link between the price of potassium chloride and of various complex fertilizers, but also at the structure of the potash supply in the US market, highlighting the existence of a German export monopoly in the early twentieth century, the agreement strategies between German and French producers until 1939, and then oligopolistic competition prevailing on world markets. While many factors naturally explain the potash price evolution, it is important to recognize that the evolution of this mineral’s market structure -and consequently the strategic game between producing companies- is also among the best predictors. The latest market developments are a recent example.

Figure 2: Evolution of fertilizer prices (In current USD per metric ton)

The World Bank (the pink sheet)

The potash market conditions are now like the other commodity markets: hardly dynamic. The Canadian group Potash Corp. of Saskatchewan (PCS), the largest fertilizer producer (by volume) experienced a drop in sales volume by almost 30% in the fourth quarter of 2015 compared to the previous year. The explanation for this price decline is multiple, combining supply and demand factors. On the demand side, the slowdown in growth in emerging countries weighed on these countries’ agricultural sectors through lower crop prices that in turn negatively affects the demand for fertilizers.This demand actually increases, but at a pace too weak to cope with excess supply. Moreover, the difficulty of access to credit in some countries like Brazil, an agricultural giant, has altered farmers' financing capacity. Fertilizer demand is consequently weakened. Exchange rate dynamics also dampen the potash market. The stronger US dollar, particularly against the Brazilian real, increases the cost of fertilizer for local producers. As noted by Tilton (1992) to be one of the important variables influencing the demand for mineral ores, the state subsidy policy for the purchase of fertilizers must also be taken into account, particularly in India, in order to explain that a drop in prices does not necessarily result in an increase in consumption. In March 2014, India reduced the subsidy on the purchase of potash by almost 20%, and in its budget the amounts allocated to alleviate the purchase cost for potash and phosphate is now reduced by 13%. In the shorter term, weather factors may also play their part. In 2015, a hot and humid summer in the United States has in particular diminished the need for fertilizers.

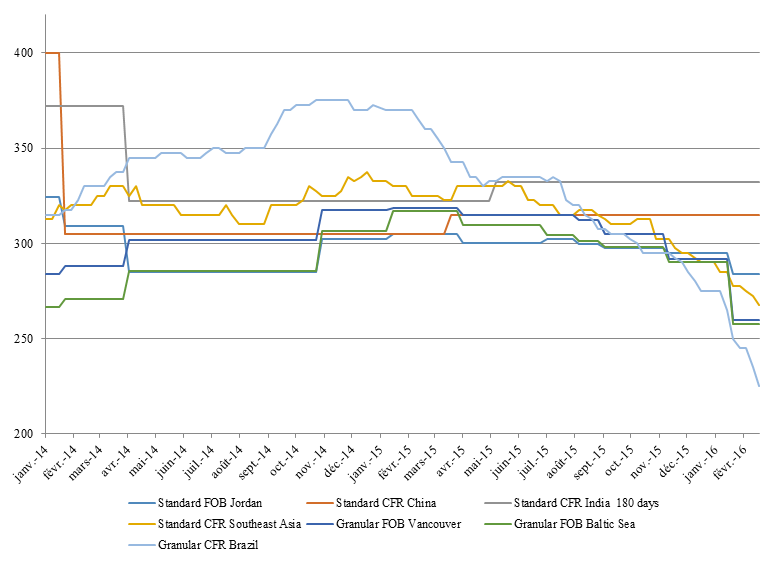

Figure 3: Potash prices by origin / destination (In current USD per metric ton)

Source: CRU

On the supply side, producers’ inability to stabilize supply, or their unwillingness to do so, is the issue. The company Belaruskali is not foreign to the current market conditions, pushing prices down in a strategy, often considered aggressive, to maintain or even increase market share. In March 2015, the signing of a potash sales contract for the Chinese market at 315 USD per ton by the Belarusian company did not fail to attract the opprobrium of its competitors on the grounds that such a pricing policy was likely to heavily penalize all producers. Rightly so: prices have since fallen to a low of 235 USD per ton for granular muriate of potash in Brazil (Figure 3). Indeed, Belaruskali’s aggressive policy does not only apply to emerging markets. Since December 2014, the group has sold over 170,000 tons of potash in the US market. It does not only take a short term approach either: The Petrikov mine, which should be operational in 2019, will increase the Belarusian company's production capacity by three million tons by 2024. If the strategies adopted by other potash giants persist, combining the closure of some mines and other developments, the market equilibrium will be negatively impacted.

The strategy pursued by Belaruskali has its roots in the July 2013 breakup between the Belarusian company and the Russian group Uralkali, which had formed a cartel known as BPC (Belarusian Potash Company), like Canpotex, its counterpart across the Atlantic in charge of PCS exports and two other north American producers, Mosaic and Agrium. The reason is simple: at that time, Uralkali wanted to increase its market share (Al Rawashdeh and Maxwell, 2014). Although the end of BPC may have often been seen as a major breakthrough, it must be recognized that tensions within the industry are not a rare reality: in 2010, the mining giant BHP Billiton launched a hostile bid to acquire PCS, which would result in failure. It was also not limited to transatlantic opposition as Pickett et al. noted (1991). In 1987 U.S. producers accused their Canadian counterparts of pursuing a dumping strategy in the United States, thus leading the government to impose a countervailing charge on Canadian imports.

The past and present potash market situation ultimately raises a question familiar to economists to which history seems to have given an unvarying response: can we sustainably influence the price of raw materials, either renewable or non-renewable, by managing the supply? In other words, can an oligopoly "in agreement" survive in the long term? The answer is almost always negative for at least three reasons. First, the relative price inelasticity of short-term supply induces price changes that sometimes favor the entry of new players attracted by higher prices that reduce de facto the entry barriers, sometimes generating losses promoting the adoption of uncooperative behavior, like what can be seen today. This is even more true as the supply level is in large part determined by investment decisions made several years ago and a priori are not part of an implicit understanding that might occur in the short term concerning the production and storage levels. The debt resulting from this investment policy -often excessive in a context of a price boom- also impacts the adoption of a strategy to offset falling prices, when it occurs, by increasing the volume sold in markets. Furthermore, market regulation by adjusting the volume requires agreement on the remunerative price aspect, which, although it may make sense from an economic point of view, is actually very different from one company (or a nation) to another. It is important to remember that ultimately the notion of "cartel," often eagerly used to describe a situation dominated by a small number of producers, only is valid if the consumer bargaining power is non-existent or limited, which hardly seems to be the case with potash, as with other fertilizers. Such a finding does not mean that producers cannot periodically influence prices, either directly through their business practices or indirectly by their ability to alter the behavior of other players in the sector. However, it is the permanence of their influence that is in question. Because of the degree of concentration upstream and downstream of the industry and temporal discontinuity in the market, it is very probable that the ability to "shape" the price is sometimes on the buyer side, and sometimes on the producer side.

In this anthropic context, it seems difficult to make solid predictions about the sector’s future. A remark is however necessary. Although attempts have been undertaken in this sense, particularly in the United States, the fertilizer markets are distinctive in that they have not been sustainably financialized, unlike almost all agricultural commodities. While fertilizer swaps have existed for several years, with increased price volatility, which would be characterized by a loss of producer market power, buyers could eventually change the situation and lead some "commodity exchanges" to experiment with futures contracts with this type of underlying assets. Producers would then have little to gain from what is akin to a revolution: a factor to perhaps take into consideration in the context of a price war.