Changes in The Commodities Market - Part 3: what implications for producers and end users?

For several months, the economic and political spheres have been focused on raw materials, questioning the lev-els that oil prices will reach in the mid-term. This will not surprise anyone: the primary concern of many agricultur-al, industrial or transport sectors is the commodities dy-namic, which may alone have a significant impact on firms’ profitability, whether they produce or use these products. The end of the "super cycle" of commodities, including the price collapse of crude oil or of base metals is only one manifestation, which has helped to rebalance the strategic relationship between buyers and sellers: end-users in this recession experience a boost, while producers are seeing their margins shrink and consequently post-pone their investment projects. This is however not the only key. As mentioned above, another key is the with-drawal of the western banks from the commodity sector and the rise of international traders, particularly in Asia. Herein lies the paradigm shift. The fear of economic or financial consequences of such a mutation for producers and users is in itself essential. One cannot safely make an assertion since both channels of commodities are different and the situation of each company involved is unique. Two assertions are nevertheless possible: The financial commodity markets are significantly stronger and those who do not have the culture to understand them or the means to access them and techniques to use them could be heavily penalized.

In a context of re-regulation of the banking sector and financial markets, the first of these statements cannot fail to surprise. And yet, we need to be convinced of its mer-its, and remember that the economic utility of the finan-cial markets is not only shares or bond markets, and that one of their functions is, beyond financing the economy, to organize the transfer of risk. These, of whatever nature, arise from the requirement (economic, legal or financial) that an economic agent has to perform an operation in the future within conditions beyond its control: sell listed shares, go into debt at variable rates, pay an invoice in foreign currency, buy oil or sell a future harvest of wheat, etc.

Faced with these various risks, the financial derivatives markets (options, swaps, futures) are not a solution, neither immediate nor optimal, and never will be. Negotiating long-term agreements, risk pooling, building up buffer stocks, implementing stabilization or compensation funds, such as what is done in Morocco and also in India, Egypt and Ghana, are all examples of various strategies that can be implemented within a company or across a country,sometimes to protect producers, sometimes consumers, including households, from excessive fluctuations in the price of commodities. These different approaches, however, have three drawbacks: they are traditionally not very flexible, have a financial cost and therefore often designed primarily to better spread the risk between the different stakeholders in the sector, which is in practice not always possible. Basically, this means that there is indeed, within a sector, buyers and sellers with equivalent financial constraints and opposite risk profiles: wheat producers, called "long" (i.e. they are potential sellers according to current finance terminology, and are willing to protect themselves from future price decreases) would thus have millers to contend with, who are structurally "short" (i.e. potential buyers) and concerned with protecting themselves from higher wheat prices. The situation is ideal and leads to the negotiation of a futures price established on a commercial basis. The reality is often different: the only asymmetry between buyers and sellers may well be enough to condemn this exchange because the price cannot be satisfactory for both counterparts. The derivatives markets aim to outsource a portion of a sector’s price risk that it fails to internalize. This role is consistently confirmed since the launch of the first modern financial futures markets in Chicago in the mid-nineteenth century. Salmon, milk, and plastic are among the recent examples of new futures contracts launched around the world, in the United States, Europe, and China. We could convince ourselves locally that this unique mode of risk management is not the proper approach. However, the expansion dynamics of financial commodity markets internationally will continue. The use of derivatives for hedging purposes can no longer be ignored.

It seems reasonable that all agents should have direct or indirect access to derivative commodity markets if their resulting business and financial risks (interest rate, foreign exchange, commodities) warrant it. Significant differences exist in this respect between countries, sectors and types of businesses. Some countries, like the US, UK or, more recently, China, placed the derivatives markets at the center of commodities sectors. Other countries did not. In the latter case, access to international financial markets may be particularly difficult for the whole economy and, especially when exchange controls exist. It is important to remember the strategic importance of a commodity exchange for an economy: its sole objective is not only to offer risk management solutions; it also promotes the emergence of a reference price, which tends to impose itself internationally and gives a considerable comparative advantage in the sector in the host country. It is thus no accident that China, the world's largest steel producer, has launched a contract on iron ore on the Dalian Commodity Exchange in 2013, pushing the traditional markets such as the Chicago Mercantile Exchange to consequently adopt a Chinese price reference. Some sectors will not have a similar need to resort to financial markets, while others, like most agricultural sectors grains, protein and oleaginous products or soft commodities (coffee, sugar, cocoa, cotton) rely heavily on futures contracts and other risk management instruments. In the latter case, significant differences remain between companies with regard to their ability to respond.

Those with a broad financial base will naturally have little or no constraints in using them, either because they directly access the commodity exchange as a member, or because the constraints of prudential regulation hardly affect them. The observed vertical integration phenomenon in the commodities markets that proceed a downward movement, from upstream to downstream, as well as an upward movement, also strengthens their capacity to respond. For the smallest of them, however,access to capital markets is reduced due to the phasing out of banks from the commodities risk management segment and / or greater regulatory constraints.

Access to financial markets is only meaningful if the opportunities they offer are fully understood. This requires that economic agents likely to use these markets precisely understand the risk cover-age (or "hedging"), the objectives and limits, as well as the costs and the risks they entail. This is where the culture of financial markets matters most.

The 3 key elements of the risk-management culture

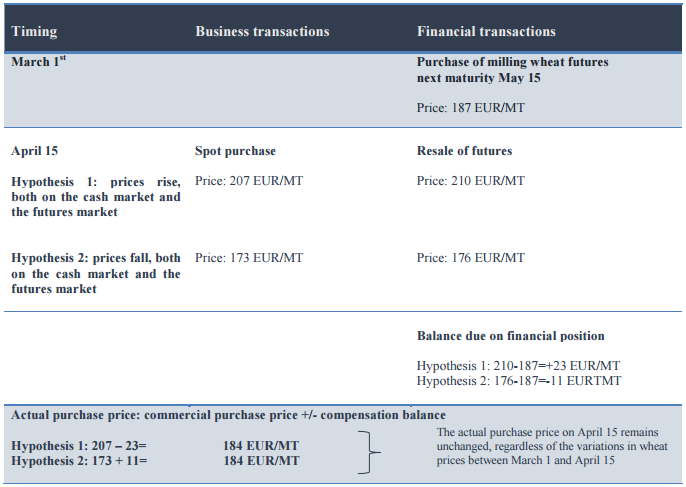

It can be roughly summarized in three points. Assume that a purchase and sale transaction of a derivative (like any other asset) cannot be systematically considered as a speculative transaction. From a general and fundamental point of view, hedging risk consists of creating a financial position (long or short) that will have a positive pay-off if the hedging agent’s initial position (i.e. commercial) generates losses (and vice versa). The company’s net income becomes less sensitive to fluctuations in the risk of commodities. To do so, a user who must buy at t+n and fears higher prices at t0 can buy a futures contract and sell it at t+n the exact moment when his business transaction takes place (see Table 1). The actual purchase price is then independent of the market price prevailing at t+n, under the assumption of an unchanged basis.

Table 1: Simplified example of a hedging purchase of wheat futures contracts

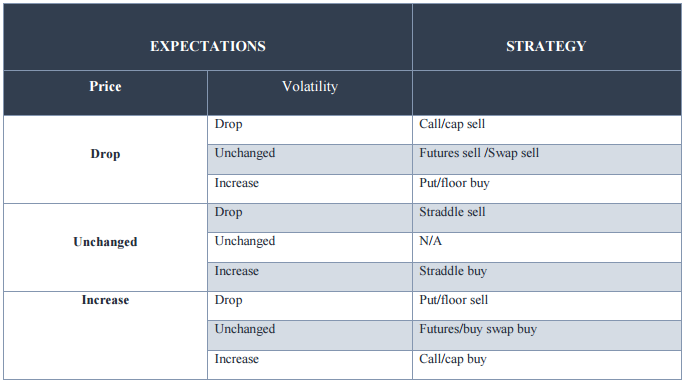

It is also important to remember that the use of derivatives is not based on any real certainty or some learned pat-tern, but is a matter of choice and expectations. A second example: in its simplest form, hedging a risk by buying a swap amounts to considering that the price conditions prevailing in t0 are more interesting than those that pre-vail in t+n and that therefore better to be established immediately in order to benefit in the future. A swap buyer locks in the price at which it will buy the raw material that it requires for its economic activity over the coming months. In contrast, doing nothing to address this risk means that the buyer speculates that the market conditions will be more favorable in the future. However, there is no evidence at t0 that one solution is, in absolute terms, better then the other, and the financial consequences of a mistake can be as heavy as one that is hedged than one that is speculated. Thus, choosing a hedging strategy requires finding a financial strategy tailored to our expecta-tions about the level and volatility of the price of the material that we buy or we sell (see Table 2), as well as un-derstanding the financial consequences of an erroneous expectation. Unlike a swap, a "call" or "cap" option al-lows to set a maximum purchase price and widely limit the cost of an expectations error. In case of a drop in the price of the raw material, a swap buyer is indeed obliged to buy at the contracted fixed price, while the cap buyer will benefit from the lower prices. The latter strategy is not without its constraints. A call option on oil products will thus be even more expensive than expected volatility in crude prices will be. Just like a car that is by nature always more comfortable and safer than a bicycle, but also much less economical and sometimes unprofitable, an option is always more flexible than a swap, but its cost is also higher.

Table 2: Market expectations and hedging strategy