Deindustrialization and Employment in Morocco

This policy brief shows that the downward trend of employment in manufacturing in Morocco is due primarily to labor productivity improvement and that the increased deficit in manufacturing trade also plays an important role. While recognizing the crucial importance of a vibrant manufacturing sector in Morocco, this brief argues that Morocco cannot rely primarily on manufactures to “pull” labor out of agriculture. To provide more jobs, Moroccan policies should pay more attention to sectors which employ large numbers of people and where employment is expanding as a result of the ongoing structural transformation of the Moroccan economy.

As in most countries, the share of manufacturing in total output is shrinking in Morocco and the share of manufacturing employment in total employment is shrinking even faster. Besides, employment in manufacturing started declining in absolute terms since 2009 that corresponds to the onset of the 2008 worldwide economic downturn.

In advanced countries, economists consider such a trend “normal” given the low income-elasticity of manufactures as incomes rise. The share of expenditure on manufactures in total spending tends to decline paralleling – though less steeply - that of agricultural products in total expenditures. Additionally, reflecting a presumption that labor productivity advances more rapidly in manufacturing than in most services, the share of employment is expected to decline relative to services, as is the relative price of manufactures (Baumol, 1967).

However, in Morocco as in many other developing countries, the declining share of manufacturing is not considered normal. On the contrary, it raises the specter of “premature deindustrialization,” the worry that manufacturing will not enable Morocco to climb the development ladder, as had been the case of early industrializers such as Great Britain and France over the course of the 19th century and some more recent industrializers in East Asia. Moreover, Morocco’s high rates of youth unemployment, and underemployment, especially of women, means that the failure of manufacturing to generate large numbers of jobs remains an acute source of concern.

This brief aims to provide a better understanding of the causes of the decline in manufacturing employment in Morocco over a relatively short period, 2007-2015, dictated by the availability of Supply and Use Tables (SUT) required to conduct the analysis. It also happens that the debate over deindustrialization in Morocco gained momentum only in the recent period, as over 2000-2007 manufacturing employment remained broadly steady as a share of total employment, and increased by 1.5% a year in absolute terms.

The analysis over 2007-2015 shows that the relative decline of the manufacturing employment in Morocco is not due to slow domestic final demand for manufactures, and nor is it due to unfavorable trends in net intermediate demand for manufactures by other sectors of the Moroccan economy. Instead, rapidly increasing labor productivity growth in manufacturing, especially in the mechanical, metallurgical and electrical as well as agri-food sectors, account for a large portion of the decline in employment share. Morocco’s increasing trade deficit in manufactures also played a large, albeit smaller, role. Trade with China alone accounted for more than half of the deterioration in the trade deficit in manufactures. Over the period, production of textiles in Morocco declined in absolute terms, also contributing to the decline in overall manufacturing employment2.

Morocco’s trade liberalization in recent years was highly beneficial for consumers, for firms dependent on imported components and raw materials, and contributed to attract Foreign Direct Investment (FDI)3. Trade liberalization was also associated with a widening trade deficit with China and the European Union and caused markedly increased competitive pressures in manufacturing which spurred productivity growth. This observation should not be read as blaming trade opening for the sluggish growth of employment in Morocco. Instead, domestic conditions and policies, which were not adequately supportive of the country’s competitiveness, are likely the more important cause (Dadush and Myachenkova, 2018). The analysis carries some policy implications set out in the brief’s concluding section.

Why care about manufacturing?

There are five powerful reasons to care about the growth of the manufacturing sector in Morocco, as elsewhere. The manufacturing sector can be a source of high-paying, high-productivity jobs; it can be the source of rapid productivity growth spurred by innovation and international competition; it can create important forward and backward linkages; it can generate economies of scale and grow to be very large by penetrating world markets; and it can be a large source of foreign exchange (Rodrik, 2015).

Therefore, policymakers must care deeply about the evolution of the manufacturing sector. However, they must also be realistic about the sector’s potential in light of its relatively small size and low growth rate compared to services (Dadush, 2015). By the same token, policy-makers must appreciate that many service sectors are increasingly capable not only of generating large number of jobs, but also of exhibiting some of the desirable features of manufactures.

Thus, the highest paying jobs in the economy are found in finance, not in manufacturing. In fact, many “modern” service sectors, such as business services, software provision, finance, parts of retailing, etc. have been found to generate rapid labor productivity growth ; Recent studies by Mc Kinsey and others have held out the prospect of artificial intelligence vastly improving labor and capital productivity across a host of activities, including the service sector (“Artificial Intelligence the next digital frontier?” (2017). In addition, sectors such as tourism and construction generate important backward and forward linkages; increasingly, services are tradeable, and activities such as back-office service provision can address large world markets; and services such as tourism and transport can be large generators of foreign exchange, as can migrant remittances (labor services). Though services represent only about 20% of world exports expressed in gross terms, they represent about a far higher share of world exports expressed in terms of domestic value added. Moreover, manufactures exports contain a high share of imported and domestic services (Cesar et al., 2017, Banque de France Working Paper).

Dani Rodrik, a keen advocate of development through industrialization, has argued that “light” (i.e. labor intensive) manufacturing not only creates higher productivity jobs than agriculture, but is also inclusive and requires skills that are not significantly different from those in agricultural activities. Rodrik provides convincing evidence that manufacturing productivity tends to catch up to international levels, even when many of the other conditions required for broader economic development are barely met. He argues that the most successful countries have all relied on rapid industrialization.

Others have taken a more nuanced view (Dadush, 2015). While countries such as Korea have achieved spectacular growth based partly on penetration of world markets in manufactures, and all countries rely on manufactures to some extent, many countries have enjoyed less rapid but respectable growth without relying mainly on manufacturing. Thus, in recent decades, 39 economies have been able to double their per capita income over 20-30 years and have achieved large improvement in other development indicators without exhibiting a comparative advantage in manufactures or relying principally on manufacturing4. These countries include Chile, Egypt and Morocco, for example.

Of course, not every country can grow its manufacturing sector by capturing an increased market share on world markets. An efficient service sector is an essential companion to a competitive manufacturing sector, and the value added of many firms classified as belonging to the manufacturing sectors consists mainly of intangible activities which are, in fact services. The data shows that services have accounted for the lion’s share of growth even in the rapid industrializers in East Asia and elsewhere.

All that said, a vibrant manufacturing sector can be a vital contributor to the long-term development process, and every country carries out some manufacturing. To formulate a sensible policy towards manufacturing, understanding its key drivers is a first step.

The evolution of manufacturing: stylized facts of the Moroccan economy

The contribution of the manufacturing sector in Morocco to wealth creation is on a downward trend. Using real or nominal figures, the trend is the same. In fact, its share in total output at constant prices dropped from 16.3% in 2000 to 14% in 2015. In current prices, the decline is less, from 17.4% in 2000 to 16.1% in 2015. This trend is similar to that observed across low -income countries and is less sharp than that observed in middle-income countries. Still, Morocco’s share of manufacturing in GDP is lower than that of higher middle-income group, where manufactures account for more than 20% of total GDP.

The sharper decline of manufacturing at constant than current prices implies that the relative price of tradables to non-tradables in Morocco has increased. This occurred despite trade liberalization and rapid productivity growth in manufacturing. These forces may have been partly moderated by the weakening of the purchasing power of the Moroccan currency, which depreciated by 3.8%, from 2007 to 2015, and/or may have resulted from more rapid increases in wages in the manufacturing sector.

Employment in manufacturing, our focus, declined from 12.2% to 10.4% of total employment over 2000 to 2015, with an especially sharp decline between 2008 and 2015. Employment in manufacturing actually declined in absolute terms even though value added grew at 3.3% in real terms from 2007 to 2015. Over this period, labor productivity growth in the manufacturing sector outperformed that of the economy as a whole, even though it was already 20% higher than in the rest of the economy in 2007. An important contributor to this shift was the increased capital intensity of manufactures, which was also reflected in relatively slow growth of total factor productivity (TFP) or even negative growth of TFP (High Commission for Planning, 2016). The low employment intensity of manufacturing is also visible in a recent analysis by the Ministry of Economy and Finance, which shows that the employment elasticity of employment in industry is near zero, while that of construction is 0.86 and that of retailing (“commerce”) is 0.7.

These aggregates mask important sectoral shifts, as shown in Figure 7, below. Nearly half of the growth in manufacturing value added is owed to the mechanic and electronic sector, while the agri-food sector contributed one-third. Regarding the value added in garments and textiles sector, which accounts for over 40% of manufacturing employment, it has declined - the only manufacturing sector that experienced a negative growth rate. Garments and textiles suffered severe employment losses over the years, proportionately larger than the value added decline. Only the mechanics and electronic, and agri-food sectors have shown employment growth, albeit at a very slow pace.

Factors accounting for the decline in manufacturing employment: quantification

In this section, we quantify the effects on manufacturing employment in a simple accounting framework. The identity relation between employment, value added and productivity is as follows :

∆(LM) = ∆(VAM) - ∆(ProductivityM)5 (1)

Where,

VAM = Value Added in manufacturing sector

LM = Labor in the manufacturing sector

ProductivityM = VA/Labor in manufacturing sector

And, that between value added, consumption and trade is as follows:

VAM + ImportsM = Domestic Final DemandM + ExportsM + Net Intermediate DemandM (2)

Net intermediate demand stands for the domestic sectoral trade between sectors that serve as an intermediate input for sectors to produce their final output.

This equation refers to the equality between total resources of manufacturing products to total Uses, available in Supply and Uses Tables. The left hand side of the equation comprises total supply of the manufacturing products that are either produced domestically or imported. The right hand side comprises uses of manufactures, in domestic demand (including for consumption or investment purposes), and exports. The net intermediate demand term in the equation reflects the sales of intermediate parts and material of the manufacturing sector to other sectors less the purchases of parts and materials from other sectors.

By rearranging the terms of the equation, we obtain:

VAM = Domestic Final DemandM (DFDM) + net international trade balance (X-M)inter + net intermediate demand (X-M)sectoral (3)

By replacing (3) in (1), we obtain:

∆(LM) = ∆(DFDM + (X-M)inter + (X-M)sectoral)) - ∆(ProductivityM). (4)

The manufacturing employment change between two periods is accounted for by the change in total domestic demand, net trade balance and net intermediate demand, and productivity evolution. The equation is a purely descriptive identity – i.e. it is always true and does not imply or deny causality in any direction. It is nevertheless useful in quantifying the main effects operating on employment.

The Supply and Uses Table (SUT) for Morocco, which is available annually since 2007 following the new base year, can be used to quantify the terms in equation 4. This quantification poses three issues. The first one is tied to nomenclature of the SUT. Each component of the uses is expressed in purchasing prices that includes margins and taxes, while total resources are available in basic prices. We must transform total uses, valued at market prices, into economic flows valued at basic prices. The allocation of margins and indirect taxes for all users was estimated based on shares calculated from the sales structure of the Supply Table (Guilhoto & Sesso Filho, 2005). The underlying assumption is that margins coefficients and tax rates on products are the same for all users.

The second issue is tied to the necessity to extract the volume effect out of the nominal variables, as SUT are produced in current prices. We have used the consumer price index to convert nominal domestic final demand into real domestic final demand. For intermediate consumptions, the production prices index was used to convert them into constant prices, while for exports and imports, due to unavailability of manufacturing unit value index, the choice fell on imports and exports prices index provided by the World Bank database. The equality of the equation (2) was then tested. A difference between the right hand side, the left one was below 1%. We decided to divide it along each component of total uses, following their weight.

The third issue is related to the fact that some manufacturing products are produced in the non-manufacturing sector. In fact, 4% of manufactures are produced in other sectors. For example, firms in the agriculture sector produce primarily agricultural products but also some processed food products. Similarly, firms in the manufacturing sector produce some products or services that are not classified as manufacturing. We included all the manufacturing products in the analysis whatever their source, and exclude non-manufacturing output.

The resulting analysis of employment change indicates that domestic final demand for manufactures, which grew 3% a year over 2007-2015, is the key driver of manufacturing value added and employment growth in Morocco, while international trade affected manufacturing employment negatively, as did increased labor productivity. The accounting below shows that, other things equal, the increase in domestic final demand for manufactures nationally added over 600 thousand jobs in Morocco over 2007-2015, while net intermediate demand for manufactures by other production sectors added very little. These favorable forces on employment were offset by a notional loss of over 300 thousand jobs due to international trade and another nearly 400 thousand jobs due to automation, reallocation, and other sources of labor productivity improvement. Over the period, manufacturing employment in Morocco declined by over 80 thousand jobs.6

The Trade Effect

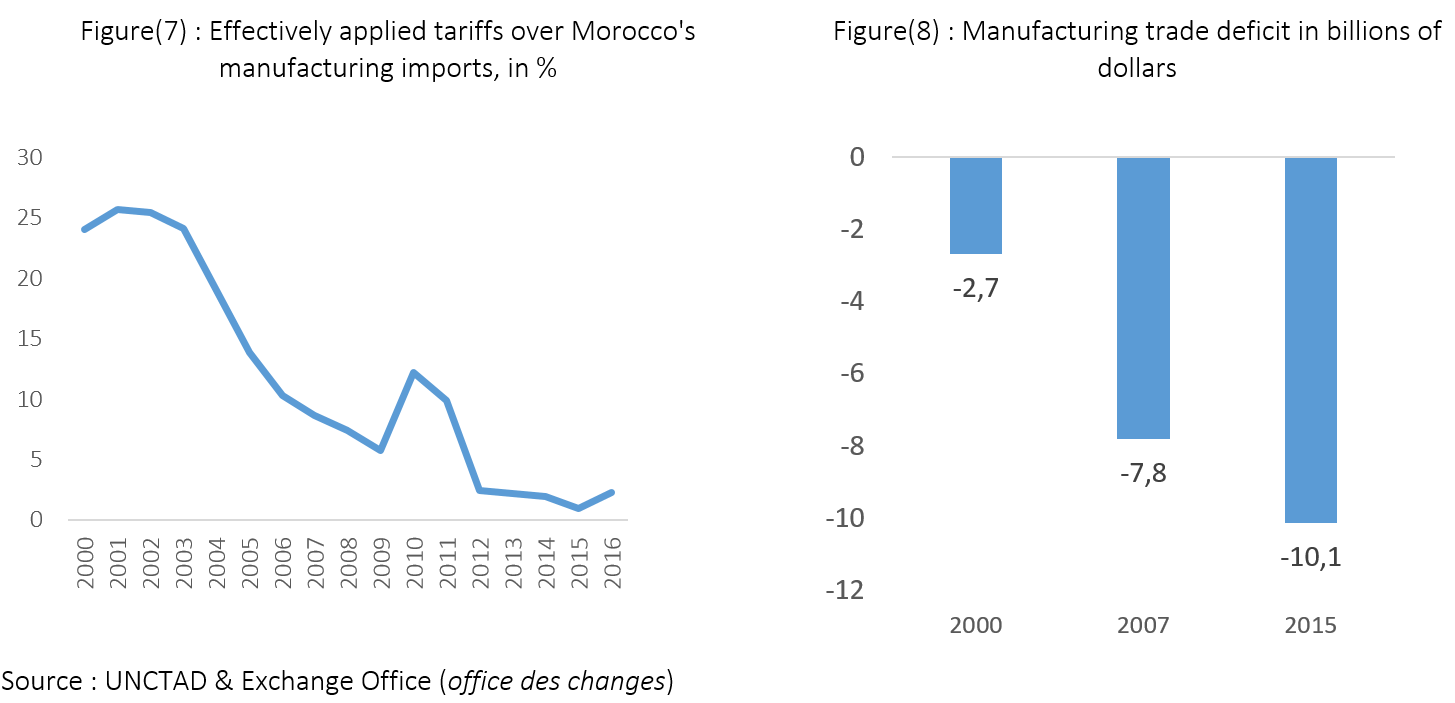

The positive dynamic of domestic final demand for manufactures was not reflected in proportional increases of domestic production, as import penetration increased from 35.7% in 2007 to 36.2% in 2015, while exports ratio to total resources stayed unchanged at 16.9%.7 Over this period, the Moroccan economy became increasingly open, as effectively applied tariffs on manufactured goods declined from 8.7% in 2007 to 2.3% in 2016. The trade deficit in manufactures increased by 31% in real terms during this period, implicitly accounting for losses of nearly 318,000 jobs.

These employment losses were driven mainly by the increasing bilateral deficit with the Chinese, German, Turkish and Portuguese economies. As Table (1) above shows, China alone accounted for over half the deterioration in Morocco’s trade deficit in manufactures over the period. Increased imports of textile and clothing and electrical equipment accounted for most of the increase in the bilateral trade deficit with China and Turkey. In addition, increased imports of textile and clothing help explain the large employment decline in that sector. Transport equipment accounted for most of the increase of the bilateral trade deficit with Germany. Morocco’s trade balance in manufactures increased (rising surplus or shrinking deficit) with a diverse group of countries, most often on account of fertilizers, a part of the chemical industry. The large reduction of Morocco’s trade deficit with Spain is accounted for garments and electrical equipment. Morocco’s exports of intermediate goods have grown significantly, an indicator of the economy’s integration in global value chains.

Morocco is not alone in seeing its manufactures trade deficit deteriorate sharply over the period under consideration. Manufactures deficits have deteriorated or surpluses have shrunk in over two thirds of the countries in our sample, while only one third were able to increase their manufactures surpluses or reduce their deficits.9 Besides the United States, the list of the top ten of the most widening manufacturing deficits is comprised majorly of oil exporters. Among countries that ran increased manufactures trade surpluses, China stands out, having increased its surplus by 615 billion dollars over a relatively short period. Morocco is too small to feature among the largest changes in manufactures trade balance, but, expressed as a share of its GDP, the deterioration amounts to 2.7%, a major shift, comparable with those of much larger economies, and larger proportionally than that of the United States.

.png)

The Productivity Effect

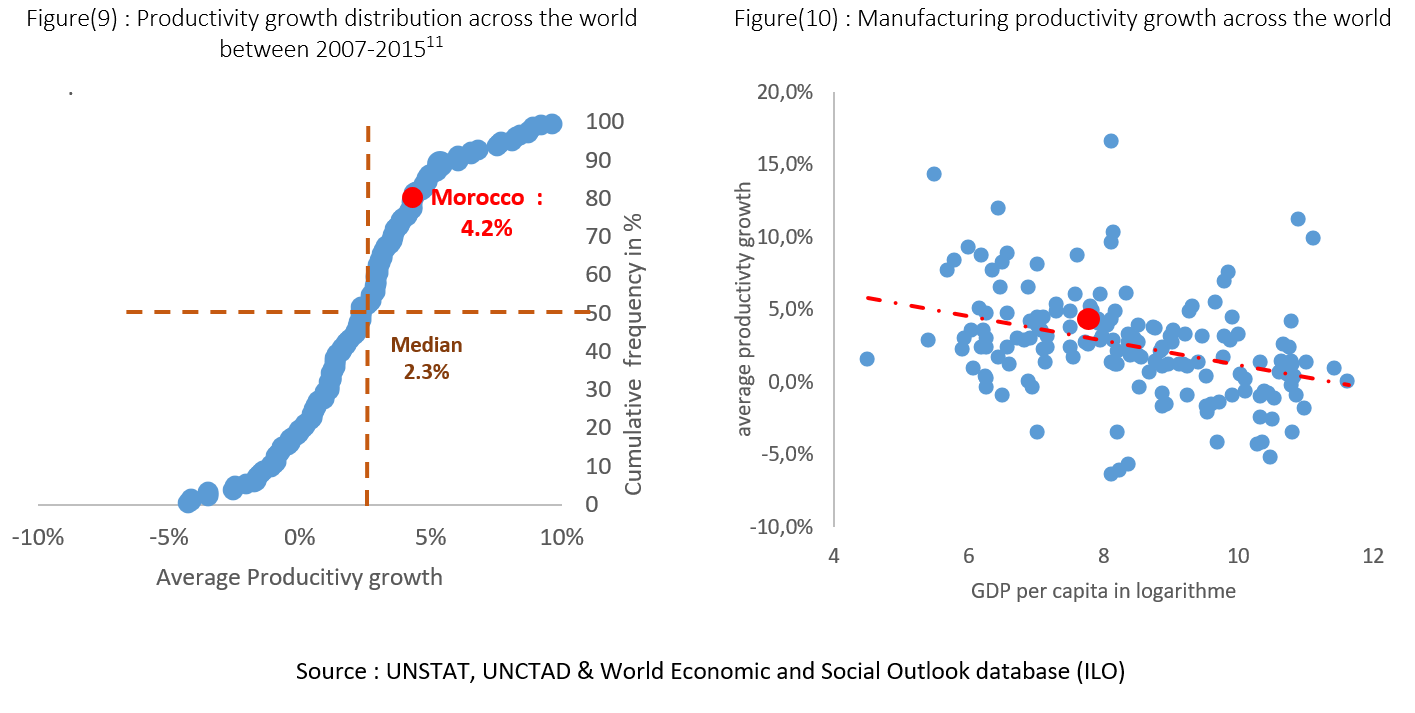

Though shifting trade patterns contributed in a major way, the large labor productivity gains within the Moroccan manufacturing sector are the single most important factor accounting for the employment decline. These productivity gains also outstripped those in the service sector. Increased trade and increased productivity are clearly interrelated, as domestic firms supplying the domestic or foreign market, and increasingly exposed to foreign competition, are forced to upgrade and operate at international standards. This process frequently involves automation and a more sparing use of labor. Companies that rely most heavily on exports must serve an international clientele, which demands high and predictable quality, on-time delivery, etc., and are even more subject to these modernization trends. One benefit is that the attractiveness of the Moroccan economy to manufacturing companies appears to have increased in the last decade, as Foreign Direct Investments (FDI) inflow to manufacturing has outperformed other prominent sectors, such as the financial sector, tourism, and the real estate sector, especially between 2012 and 2014. The attractiveness of the Moroccan economy may improve further as it deepens its ties with its neighbors in Sub-Saharan Africa, which represent some of the fastest growing populations in the world.

The improvement of manufacturing productivity in Morocco is also striking in international comparison. Indeed, some 80% of economies exhibit lower manufacturing productivity growth than Morocco’s (figure 10). Morocco’s manufacturing sector also outperformed countries with similar level of GDP per capita (figure 11).

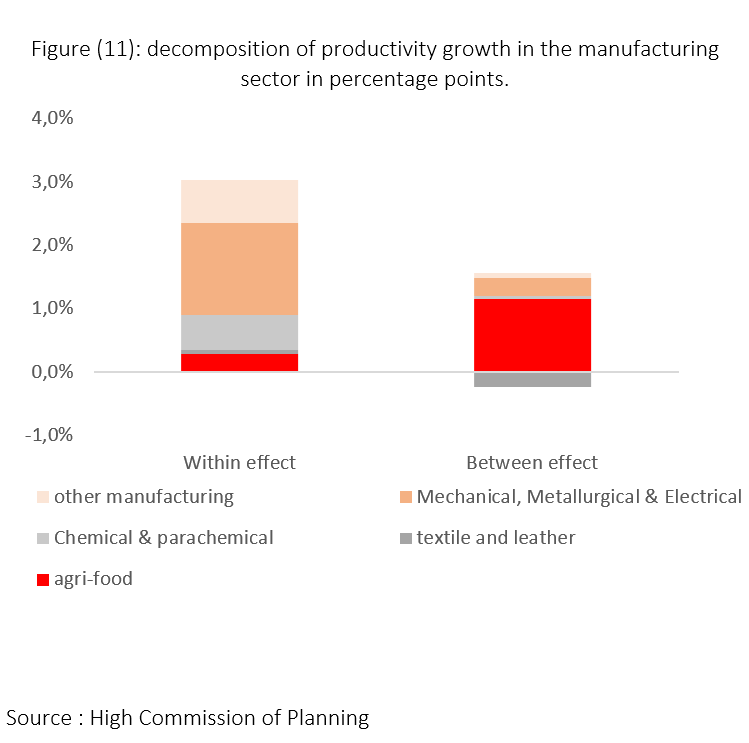

The manufacturing sector in Morocco has experienced significant restructuring, moving away from sectors with low productivity levels to higher productivity sectors. To assess the extent to which reallocation within the sector has contributed to productivity growth, we have distinguished between “within” sector productivity improvement and that due to moving from low to high productivity sectors, or “between” sectors (Rodrick and McMillan, 2011). The large mechanical, metallurgical and electrical sectors account for most of the “within” productivity increase followed by Chemical and Para-chemical industries. Reallocation of labor from textiles and garments, towards the agri-food business and the mechanical, metallurgical and electrical sector boosted the “between” component of productivity increase.

It should be noted that while the data to carry out the same detailed analysis is not available over a longer period, results over 2000-2007 confirm broadly the prominent roles of productivity gains and widening trade deficits in affecting manufacturing employment, which, however, grew over the period. Productivity gains were less, at 2.2% a year and below the average of the whole economy, but the manufacturing trade deficit deteriorated even more rapidly over 2000-2007 than it did over the more recent period.

Policy

The objective of this brief is limited to an accounting of the proximate causes of the decline of manufacturing employment in Morocco. To elaborate, the paper does not delve deeply into the underlying causes of the rapid labor productivity increase in manufacturing, which – even though it means less jobs in manufacturing – is an encouraging phenomenon indistinguishable from successful development. Nor does it analyze the deeper causes of the decline in the trade balance. This feature is, on the face of it, less encouraging, since it signals the difficulties that Moroccan firms have in confronting international competition. However, one must also recall that it reflects the availability of cheaper international products for consumers and importing firms and is partly the result of deliberate policies of trade liberalization, which can be expected to have important growth-enhancing effects in the long run. Insofar as the increased trade deficit in manufactures is the mirror image of inflows of foreign direct investment and of capital destined to long-term investment in Morocco, it could even represent a promising development. We leave these important questions to future research.

Even with these evident limitations, the analysis clearly confirms that, on current trends, or even with sizable improvement in these trends, Morocco cannot rely principally on manufacturing to pull labor out of agriculture. The latter still represent some 37% of total employment, compared with about 10% in manufactures, a sector where employment is declining. While demand for manufactures in Morocco is likely to continue to grow rapidly, supporting jobs in the sector, there is little indication that labor productivity growth in manufacturing is likely to slow down sharply (thus requiring more workers per unit of output) – and, nor would that be desirable. Given the manufacturing sector’s modest size, even a sizable shift in the trade balance in manufactures is unlikely to materially change the sector’s weight in employment in the foreseeable future.

That said, the importance of a vibrant manufacturing sector in Morocco is evident for all the reasons set out in the introduction. This analysis thus underscores the need for policies that enable the manufacturing sector to remain internationally competitive, so that, at least, employment in that sector does not decline further.

The analysis also points to the centrality of policies that enhance the expansion of employment in services. In Morocco, traded and labor-intensive services such as tourism and back-office remote service provision appear to be especially promising. Labor-intensive activities such as construction and retailing may not appear as promising, since they earn little foreign exchange, but they can be a very important part of a job creation strategy that rests on multiple pillars. In this regard, Morocco is fortunate in being able to rely on multiple sources of foreign exchange, ranging from migrant remittances to phosphates. Thus, to provide more jobs, Moroccan policies should in a sense “go with the flow,” paying more attention to those sectors which employ large numbers of people and where employment is expanding as a result of the ongoing structural transformation of the Moroccan economy. Such a strategy is not a substitute for, but fully consistent with, continued efforts to enhance the competitiveness of Morocco’s manufacturing.

***

1 - The authors wish to thank Said Moufti for detailed and insightful comments on an earlier version of the paper.

2 - The deeper causes of slow job creation in recent years relate to the global financial crisis which affected Morocco, albeit modestly, and other cyclical forces which account for below-potential growth. The formal labor market in Morocco also shows low flexibility according to the World Bank's "Doing Business" report. SMEs play a large role in the Moroccan economy, reflecting a high rate of business creation, but many do not survive and very few grow to become large employers.

3 - Dadush and Myachenkova “Assessing the EU-North Africa Trade Agreements” (2018), Bruegel and OCP Policy Center.

4 - Uri Dadush (2015) “Is Manufacturing Still a Key to Growth?” OCP Policy Center.

5 - Productivity = VA/Labor

6 - This table computes only the direct effect of forces on manufacturing employment. It is possible that a full-fledged general equilibrium analysis such as could be done by inverting an input-output matrix would yield somewhat different results, although these differences are unlikely to be large given the high level of aggregation used in this exercise.

7 - Nominal exports have grown by 81% between 2007 and 2015, around half of the increase is owed to prices. This explains partially the stability of export ratio to total available resources in real terms.

8 - These numbers can be interpreted as follows: 61% of the widening total deficit in manufacturing products (MAD 23.2 billions) is vis-à-vis China. When the number is positive, it means that the bilateral deficit has shrinked or that the bilateral surplus has increased.

9 - Data for trade balance and GDP in 2015 were available for 208 countries and territories.

10 - ((X-M)2015 – (X-M)2007))/GDP2015.

The ranking is based over the change in the manufactures trade balance expressed in dollars and not in percentage change.

11 - Initially, the sample included 177 country. We used box-and-whisker plot to exclude the outliers, within the sample. An outlier is identified being larger than the third quartile by at least 1.5 times the interquartile range (Q3 – Q1), or smaller than first quartile by at least 1.5 times the interquartile range.