Policy Response to the Plunge in Oil Prices

The plunge in oil prices will only stimulate global and national aggregate demand if it is passed through to consumers. However, pass-through may be limited this time because of fiscal constraints, environmental concerns, and the need to rein in wasteful and regressive energy subsidies. Oligopolies may also appropriate a disproportionate share of the rents. The best course is to maintain high oil product prices at home by reducing energy subsidies or increasing taxes while temporarily raising income transfers to households.

Sharp surges in oil prices have preceded nearly all global recessions since World War 2, and the expectation is that plunging oil prices will have the reverse effect – that is, boost global aggregate demand and help consolidate the global recovery. Most estimates place the effect of a 50% fall in the oil price in a range of 0.5% to 1% faster global growth in 2015. But the global expansionary effect of lower oil prices may not live up to its billing if lower oil prices are not allowed to pass through to consumers and final users. As it turns out, there are a number of reasons at present why this pass-through could be limited. Most countries are contending with large budget deficits and higher debts in the wake of a still-lingering financial crisis and will want to take the opportunity to cut energy subsidies or increase taxes on oil products. Environmental concerns also argue in this direction. As always, oligopolistic firms will be tempted to capture a large share of the rents from lower oil prices.

This note argues that there is a strong likelihood that lower oil prices are here to stay for many years, and this means that both oil exporters and importers will have to undertake significant adjustment. To sustain the fragile economic recovery this year and next, policy must ensure that a significant part of the benefits of lower oil prices flow to consumers. This is important at both the global level, and at the level of individual countries. However, it is not necessary that the gains to consumers should take the form of lower prices of oil products – temporary income transfers are preferable for many reasons. Policy-makers also need to pay close attention to the micro-economic effects of lower oil prices, and in particular the possibility that oligopolistic firms, such as public utilities, airlines, refiners, and distributors, appropriate a disproportionate share of the rents from lower oil prices. There are also implications of lower oil prices for financial supervision and for monetary and exchange rate policy.

The mixed blessing of lower oil prices

The effects of lower oil prices on the global economy, and on individual economies, are complex. This is because the plunge in oil prices represents a very large transfer, amounting to some 1.5% - 2% of world GDP, from producers to consumers, and also because the reaction time of different players varies. One way to summarize these effects is to spell out four reasons why lower oil prices are a mixed blessing.

Figure 1: Spot Prices for crude oil and Short Term Economic Outlook (STEO) price forecast

Source: US Energy Information Administration

The first reason lower oil prices are a mixed blessing is that they can provide a significant boost to global aggregate demand in the short run, but with a payback in the form of slower growth later, typically assumed to occur within a year or two. Lower oil prices will tend to boost global demand in the short-run because they redistribute income from oil producers, which are heavily concentrated, and are often (not always) relatively affluent and exhibit a high propensity to save, towards oil consumers who are more likely to spend it. Lower oil prices also reduce inflationary pressures and so give more leeway to central banks to maintain loose monetary policies. However, while the real income gains of oil consumers, and the corresponding losses of oil producers, remain so long as the new price configuration holds, the global demand stimulus from lower oil prices is by its nature, time-bound and likely to be reversed. This is because, eventually oil producers adjust to the loss of income implied by lower oil prices by reducing their consumption and their investment in new oil production. The size and duration of the global stimulus before the payback period begins depends critically on the extent and speed at which consumers see the gains from lower oil prices accrue to them, and the rapidity with which oil producers adjust their spending to the shock. Since the current global recovery is fragile and many economies are operating well below potential, it is important to make sure that a sizable part of the oil windfall is spent.

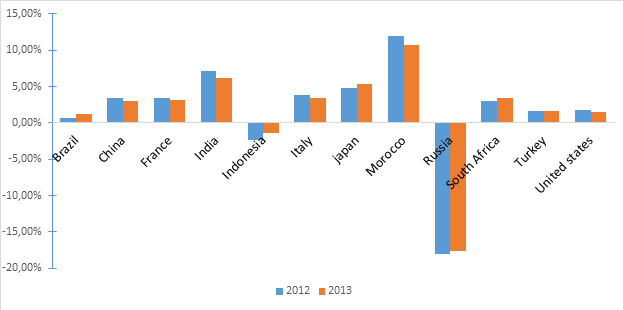

Still, even when the stimulus from lower prices is eventually reversed, as oil exporters and producers cut back, oil importers can see a lasting boost to their real income, and also to their domestic demand in so far as the windfall is spent. The size of the gain will also depend on the size of the domestic oil production sector. Take three examples of likely net gainers in the long as well as the short-term. In the US, where net oil imports are only around 1.5% of GDP, consumers are seeing a large part of the oil price decline reflected in sharply lower gasoline and other oil product prices, and this is estimated to more than offset the negative effect on the investment of the nation’s large oil production sector. In Europe, on the other hand, the oil production sector is relatively small, and net oil imports are much larger than in the US, nearer 3% of GDP. However, consumers are seeing more modest gains than in the US because of the weakening Euro and because many countries apply fixed (specific) taxes on gasoline in addition to their ad valorem taxes. In Morocco, which has essentially no oil production and where oil imports are very large as a share of GDP, 10%, the gains in aggregate demand are potentially very large, but are being mitigated to a considerable degree by the devaluation of the Dirham against the US dollar and by the government’s well-grounded decision to reduce oil subsidies and change its oil price indexation system.

Figure 2: Share of net oil imports in GDP

Source: ComTrade data, own calculations

As a general proposition, the fact that oil is priced in dollars and that the surge in oil prices has coincided with a much stronger dollar – which has appreciated by some 10-15 % in effective terms over the last year, means that the real effect on both oil exporters and importers of lower oil prices is smaller than the headlines suggest. Only the United States, and oil importers such as China which have seen little change in the exchange rate, are seeing the full effect of lower dollar-denominated oil prices.

The second reason why lower oil prices are a mixed blessing is that, unless offset by new production and user technologies or other structural shifts that affect the demand and supply of oil, lower oil prices will eventually cause markets to tighten again. This is also where the greatest uncertainty facing policy-makers lies: is the decline in oil prices likely to prove long lasting – as in the period 1986-2001, which means that they must make major adjustments, or is it going to be a relatively short-lived episode of a year or two, which means they can ride it through? We come back to this important question below.

The third reason lower oil prices are a mixed blessing is that they add to uncertainty in financial markets as well as in macroeconomic performance. This is reflected in the dimmer growth forecasts, surging yields and prices of credit default swaps for countries from Russia to Nigeria. It is also reflected in the lower stock prices and higher bond yields of companies in the energy sector. For example, energy companies (which include many shale gas and oil producers) account for about 15% of the junk bonds issued in the United States, resulting in their weak overall performance in recent months. In Brazil, the financial troubles of Petrobras – the huge national energy company - are a major concern. The corruption scandal surrounding the company is just one illustration of the enormous potential for rent-seeking in the oil sector.

The fourth reason why lower oil prices are a mixed blessing is that they potentially stimulate the demand and use of polluting oil and other fossil fuels whose prices are correlated with oil – this effect is already highly visible in the sharp increase in US gasoline consumption, for example. Increased use of fossil fuels accelerates the accumulation of carbon in the atmosphere, while simultaneously reducing the expected profitability of alternative sources of clean energy such as wind, solar, and hydroelectric.

The 2014-2015 Oil Shock: Temporary or Permanent?

Understandably, given the size and suddenness of the shock, analysts have paid much attention to what caused the plunge in oil prices in the Fall of 2014 in the first place. Was it triggered by downside demand surprises, upside supply surprises, financial speculation, or OPEC’s decision not to cut production? More or less convincing arguments have been made for each of these hypotheses, and for various combinations of them, including for all four together. But the main point is that, from the perspective of policy, identifying the precise trigger of the oil price collapse is close to irrelevant. For any country (Saudi Arabia is a possible exception), the oil price is a given: it has declined, and the consequences are pretty much the same whatever the initial cause. It is possible, for example, that the oil price plunged because the world economy was weaker by one quarter of a percentage point than most people expected (roughly the downgrading of the IMF forecast over the relevant period[1]), but for nearly all countries – whether oil importers or oil exporters – slower growth in the rest of the world has an effect on them which is of a second order of magnitude compared to oil prices.

The only exception are countries that are almost exactly self-sufficient in oil, and where –therefore- the effect of falling oil prices is close to zero by definition, Tunisia being one example. In contrast, an oil importer such as Morocco, where the oil price decline could mean a 5% improvement in real income in 2015, that effect will dwarf that of expected changes in global aggregate demand for its exports due to slower growth in Europe, its main market. The same argument applies in reverse and even more strongly for oil exporters such as Russia where oil exports in 2014 were 18% of GDP.

From a policy perspective, then, by far the more important question is whether the plunge in oil prices is cyclical or structural – temporary or long-lasting? If lower oil prices are here to stay for many years (as far as I am aware, no expert has argued that the oil price will stay low indefinitely) then everyone will need to adjust, and – especially for large oil exporters and importers – the adjustment is likely to be major. It is evident – with the benefit of abundant hindsight - that the plunge in oil prices is not an aberration but the result of forces that have built up over many years of high prices, namely massive secular declines in the oil use/GDP ratios – which are now half what they were after the first great oil shock in 1973-75, and new technologies such as fracking and horizontal drilling and not-so-new technologies such as bio-fuels that have helped expand non-OPEC oil supply by some 10 MBD over the last 15 years. Moreover, substitution of oil by other fuels, from renewables to natural gas has also played a significant role, as can be seen from the declining oil/energy use ratios. The relevant curves, which can be seen, for example in an excellent recent assessment by the Prospects Group of the World Bank, show that these shifts have been pretty steady and secular over 40 years: even during long bouts of price weakness, energy use continued to become more efficient.

As the World Bank assessment2 has argued, the current oil price plunge resembles most closely the one of 1986, which was the result of building supply and oil conservation following the big price surges of the 1970’s, rather than those associated with a global recession in 1991, 2001, or 2008. When oil prices fell by some 2/3 in 1986, they stayed low for 15 years.

It is unlikely that we will see oil prices stay so low for that long this time – both because the supply of new unconventional oil is more elastic (shale oil wells can be brought on stream faster than conventional oil and they deplete much faster) and – as a recent IMF3 note shows, the long-term marginal cost of many relatively new sources of supply such as Canadian tar sands is very high, in the $70-80 per barrel range. Nevertheless – as argued recently by the head of Exxon-Mobil, it still is likely that it will take many years for low investment to be reflected in significantly lower supply. It is also safe to assume that adoption of improved technologies of production will not stop advancing because of low oil prices, and may even accelerate. Although conditions for exploiting them are less propitious than in the United States, recent geological surveys have identified enormous untapped reserves of shale oil and gas around the world, including in Algeria, Argentina, China, and Russia.

Oil prices have already modestly recovered from their lows to reach $48 per barrel for Brent and $58 per barrel for West Texas Intermediate at the time of writing, and most analysts believe that they will settle in the $60-80 per barrel range over many years. Despite the prevalence of use of futures markets for forecasting purposes, they are a means to hedge risks rather than reliable predictors, and it is impossible to say with any confidence when oil prices will return to their previous highs. For lack of a more modern instrument, let us resort to the bible. Recall that we have just lived through seven years of very high oil prices, and that the bible speaks of the seven years of skinny cows that follow the seven years of fat cows.

Policy Response

Let us assume then, that we are looking at prices that are 30% or so lower than they were at their recent peak and that such low prices persist over the next seven years. Oil exporters will have to cut back and oil importers will have quite a bit more spending space than they had before. But how much? Standard economic analysis can provide a rough guide. It suggests that – assuming there are no credit constraints - spending should remain in line with permanent income, which is defined as national.

So, a country whose net oil exports represent 25% of GDP, and expects oil prices to be lower by 30% over 7 years would expect a fall in its wealth of roughly 50% of GDP (equal to 30% times 25% times 7, ignoring discounting). If the rate of return on wealth is 4%, spending should be reduced by somewhere between 2% to 4% a year permanently, depending on assumptions about the multiplier effect of lower oil prices on the rest of the economy. Similarly, an oil importer such as Morocco whose net oil imports represent about 10% of GDP, might be able to increase spending indefinitely by some 0.8% to 1.5 % of GDP. These shifts in spending would apply to the economy as a whole, with the burden or the benefit to be shared between the government and the private sector.

But, beyond this indicative simulation, which can be changed based on different assumptions, how should the pie be divided and how should policy respond to the contrasting effects of lower oil prices outlined above?

Here are three simple pointers for policy:

First, it is important that a large part of the benefits of lower oil prices accrue to consumers. If this does not happen, then the net effect on global aggregate demand – which currently badly needs support – as well as on demand in individual countries will be very small and could conceivably become negative, as oil exporters and producers cut back, investment in energy is deterred, while the oil windfall is captured by fiscal consolidation or in other ways, and not spent.

Second, where the fiscal space exists, it is preferable for consumers to benefit through income transfers to them rather than through lower prices for oil products. This is desirable for three reasons: the need to limit carbon emissions and to continue to encourage alternative cleaner energy sources; the need to eliminate wasteful and often regressive energy subsidies, as well as the opportunity in some instances to raise taxes on oil products; and the need to prepare for the time when oil prices surge again.

Because the expectation is that oil prices will eventually rise again, increased income transfers to consumers should be presented and structured to be temporary. They could be presented as an “oil bonus”, and take the form of temporary income or sales tax cuts, or one-time lump sum transfers to households (not increased pensions!). Oil exporters – which need to scale back across the board – should instead use the opportunity of lower oil prices to raise taxes on oil products without a compensatory transfer to consumers.

Third, at the level of microeconomic policies, countries need to step up two types of surveillance. First, they need to monitor carefully the financial health of their energy sector to ensure that the inevitable fall-out on the more fragile and indebted companies does not have broader repercussions on the financial system. Second, they need to step up their monitoring of competition in the oil sector and in the sectors that are heavy users of oil to ensure that the rents from oil prices flow to the community at large and are not monopolized or otherwise appropriated by the likes of refiners, oil distributors, public utilities and airlines.

There are also important and more complex implications of lower oil prices for monetary and exchange rate policy which we can only touch upon in this short brief. For example, the cutbacks in spending required of oil exporters can be facilitated and executed more efficiently by allowing the currency to depreciate. Large oil importers may, on the contrary, face currency appreciation pressures that would also facilitate the transfer of real incomes to their consumers.

In the case of Morocco, the weakness of the Euro – the currency of its main market - and the widening of its trade deficit in recent years would likely preclude any upward exchange rate adjustment despite the big improvement in its terms of trade.

More generally, the enormous gyrations of oil prices over the last several years only reinforce the arguments in favor of increased exchange rate flexibility. To take again the case of Morocco, a devaluation of the exchange rate would have mitigated the country’s large external imbalances during the long spell of high oil prices, and would also have allowed more room for an appreciation now, facilitating the economy’s adjustment to lower oil prices. Income transfers to low-income households – rather than energy subsidies – should be used as a complement to the flexible exchange rate to blunt the adverse social impact of extended periods of high oil prices.